SMM January 26 News:

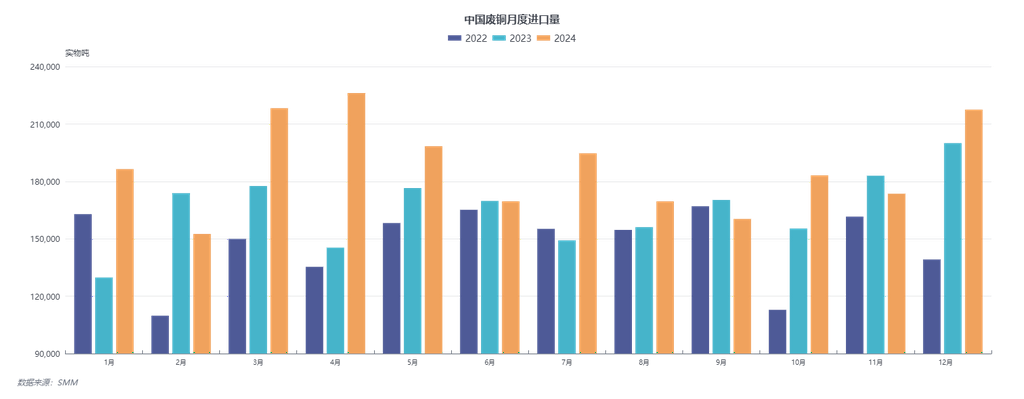

According to customs data, the total import volume of copper scrap in 2024 reached 2,249,952 mt, an increase of 13.26% YoY compared to 1,986,559 mt in 2023.

Notably, the import volumes in March, April, and December all exceeded 200,000 mt. Breaking it down, the large import volumes in March and April were mainly due to domestic importers reporting that customs had unclear classifications for certain categories of imported copper scrap at the beginning of the year, resulting in a significant number of container returns. Consequently, importers had to increase procurement volumes to ensure that import volumes did not decline sharply. Another factor driving the increase in imports was the ongoing speculation about copper concentrate supply both domestically and internationally, which pushed copper prices higher. Additionally, during March and April, smelters underwent concentrated equipment maintenance. To ensure that copper cathode production did not experience a significant pullback, the demand for externally purchased anode plates surged. Many secondary copper rod enterprises shifted to producing anode plates, and with insufficient domestic supply of raw materials for anode plate production, more enterprises turned to imported copper scrap as a supplementary raw material, leading to a spike in copper scrap imports during these months.

In December, copper scrap imports also exceeded the 200,000 mt threshold, primarily because the Chinese New Year in 2025 falls at the end of January. Import traders engaged in stockpiling in advance, intentionally increasing December's port arrivals to meet downstream procurement demand.

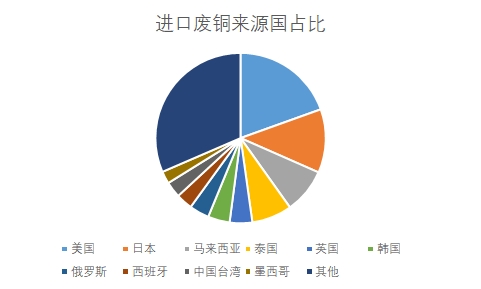

In 2024, the main sources of copper scrap imports remained the US, Japan, and Malaysia. The US accounted for 439,200 mt of imports for the year, representing 19.52% of the total. However, since January 20, when Trump assumed office as US President, he announced plans to raise tariffs on global imports to varying degrees. Based on the experience during the 2017 -2018 US-China trade war, when Chinese customs imposed a 25% tariff on US copper scrap imports in retaliation for US tariffs on Chinese exports, Chinese importers have suspended imports of secondary copper raw materials from the US since late November . It is estimated that the decline in US supply may begin in January . In Southeast Asia, since September 2024, when Malaysian customs began strengthening inspections on imported copper scrap, a large number of copper scrap containers have accumulated at ports. Some traders have had to reroute containers to Thailand for customs clearance. However, both Malaysia and Thailand have been raising the grade requirements for imported copper scrap in recent years and cracking down on the import of foreign waste due to environmental protection issues. It is expected that in 2025, China's copper scrap imports from the US and Southeast Asia will decline to varying degrees.

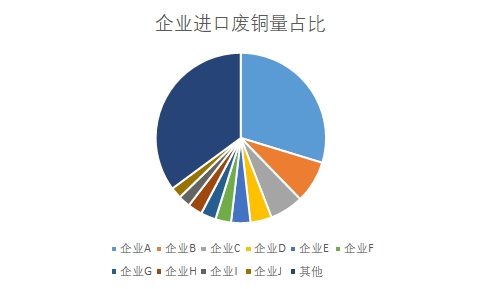

Among enterprises, Company A imported 603,800 mt of copper scrap in total for the year, accounting for 29.7% of the total. Currently, the top ten copper scrap importers in China account for 64.9% of the annual import volume, of which eight are producers and two are traders. According to interviews, producers do not use all the imported copper scrap for their own production. When copper prices rise, importers sell part of the secondary copper raw materials to earn excess profits.

In summary, due to uncertainties in US-China trade relations and stricter controls on foreign waste imports by Southeast Asian countries, copper scrap exports from these two regions to China are expected to decline to varying degrees in 2025. However, as China's secondary copper raw material supply still relies on imports, the supply-demand imbalance will be difficult to resolve in the short term.

![Sellers Held Prices Firm While Buyers Waited on the Sidelines; After the Contract Rollover, Spot Trades in the Shanghai Spot Copper Market Were Lackluster [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/HaNSH20251217171714.jpeg)